If you own a townhouse, unit, or apartment and you’re sharing common space with others, you don’t want to be left to foot the bill if there’s damage to shared parts of the building or items. But what is strata insurance, what does it cover and how do you select the right policy for your needs?

What Is Strata Insurance?

Strata Insurance, also known as Body Corporate Insurance, is a type of insurance policy designed for properties with shared spaces, such as apartment buildings, townhouses and commercial complexes in Australia. It covers the building’s common areas or shared property under the management of a strata title or body corporate entity. This insurance is mandatory in all Australian states and territories, ensuring that all unit owners are collectively protected against potential risks associated with property ownership and shared spaces.

What Does Strata Insurance Cover?

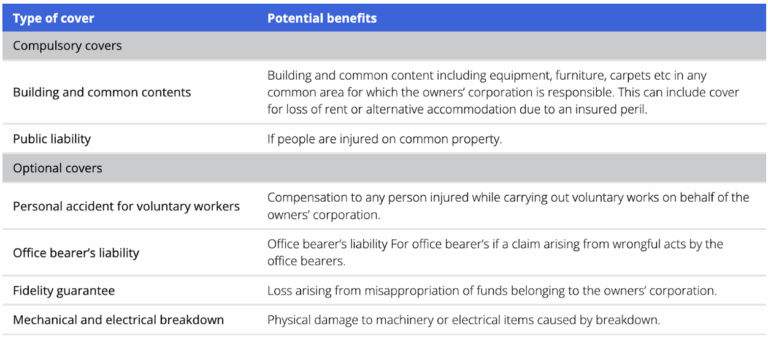

Strata insurance typically covers:

- The building itself, including permanent fixtures such as walls, ceilings, windows and balconies

- Common property such as hallways, lifts, driveways, garages, stairwells, roofs, and shared garden areas

- Public liability cover for injury or damage that occurs in common areas

- Legal liability for the owners’ corporation (body corporate)

- Common contents, such as gym equipment, shared furnishings, and lawnmowers stored on the property

For anything inside your unit or apartment, including contents, liability, or landlord protection, separate contents insurance or landlord insurance is recommended.

What Types of Properties Need Strata Insurance?

Strata title insurance is relevant for properties where ownership is divided into individual lots with shared common property. This includes:

- Apartment buildings

- Townhouse complexes

- Duplexes with shared walls

- Unit blocks

- Mixed-use buildings with both commercial and residential spaces

Why You Need a Good Strata Building Insurance Policy

Having the right strata building insurance is crucial for:

- Meeting legal obligations under your state or territory’s strata legislation

- Protecting shared property and common infrastructure from costly damage

- Safeguarding unit owners from personal liability in the event of injury or damage in shared areas

- Avoiding disputes between owners over repair and rebuilding costs

A well-structured policy ensures smooth operation of the strata scheme and peace of mind for all owners.

What’s the Difference Between Building Insurance and Strata Insurance?

Building insurance usually refers to standalone cover for a single residential home and covers the structure of the building from events like fire, storm, or accidental damage.

Strata insurance, on the other hand, is tailored for multi-unit dwellings under a strata title, where multiple owners share ownership of the building’s common areas and structure.

Key differences:

How To Find The Right Strata Insurance

With as many as 85% of recently-built strata properties having at least one known defect, according to UNSW research, the good news is that buildings with defects are still insurable.

The severity of the defects, the age of the building, outstanding legal action and any plans for defect rectification will be taken into consideration by insurers when deciding the type and extent of cover that they will offer, and the premium.

A well-tailored strata building insurance solution will also consider the building’s location, the number of tenants, the kinds of facilities and shared common areas, the reputation and track record of the building company, and the age of the building.

How AIB Insurance Can Help

At AIB Insurance, we understand that every strata complex is unique. Whether you’re a strata manager, a body corporate representative or an individual unit owner, we can help you find the right strata title insurance policy to suit your needs and budget.

Our brokers compare a range of trusted insurers and work closely with you to ensure your strata building insurance provides:

- Adequate replacement value cover

- Proper public liability limits

- Protection for shared assets and contents

- Optional extras, like catastrophe cover or machinery breakdown

With expert advice and access to tailored insurance solutions, contact our team today for simple and stress-free advice.

Important notice

This article is of a general nature only and does not take into account your specific objectives, financial situation or needs. It is also not financial advice, nor complete, so please discuss the full details with your Steadfast insurance broker as to whether these types of insurance are appropriate for you. Deductibles, exclusions and limits apply. You should consider any relevant Target Market Determination and Product Disclosure Statement in deciding whether to buy or renew these types of insurance. Various insurers issue these types of insurance and cover can differ between insurers.

Steadfast Group Ltd ACN 073 659 677

Important notice – Steadfast Group Limited ABN 98 073 659 677

This article provides information rather than financial product or other advice. The content of this article, including any information contained in it, has been prepared without taking into account your objectives, financial situation or needs. You should consider the appropriateness of the information, taking these matters into account, before you act on any information. In particular, you should review the product disclosure statement for any product that the information relates to it before acquiring the product.

Information is current as at the date the article is written as specified within it but is subject to change. Steadfast Group Ltd and Steadfast Network Brokers make no representation as to the accuracy or completeness of the information. Various third parties have contributed to the production of this content. All information is subject to copyright and may not be reproduced without the prior written consent of Steadfast Group Limited.